Most people have become tired of their 9-to-5 routine, where we are constantly under stress just to earn some money so that we can manage our bills, food, and house rent. This is a kind of “rat race” in which most of us are trapped. Sometimes there is the fear of losing our job, and sometimes the worry of paying back a loan installment. In this entire cycle, our whole life passes by until we end up in the grave.

But there is a way to escape this cycle, a path that gives us freedom of both time and money.

Here begins the FIRE (Financial Independence, Retire Early) movement. It is not a fake get-rich scheme, but a lifestyle and financial strategy whose purpose is to make you financially free before time. In this, you just need to change your financial habits, which is quite simple: save a large portion of your income, invest those savings, and reach your FIRE number where the income from your investments is enough to cover your living expenses for the rest of your life.

This is not only about retiring early, but about taking back control of your life, your time, and your finances. So that we can do what we want to do, not what this cycle forces us to do.

What Does FIRE Really Mean?

As the name suggests, FIRE has two parts: Financial Independence and Retire Early. The purpose of this movement is not to retire early but to achieve financial independence. Financial independence means that you have built your investment portfolio to such an extent that the passive income generated from it is enough to cover your yearly expenses.

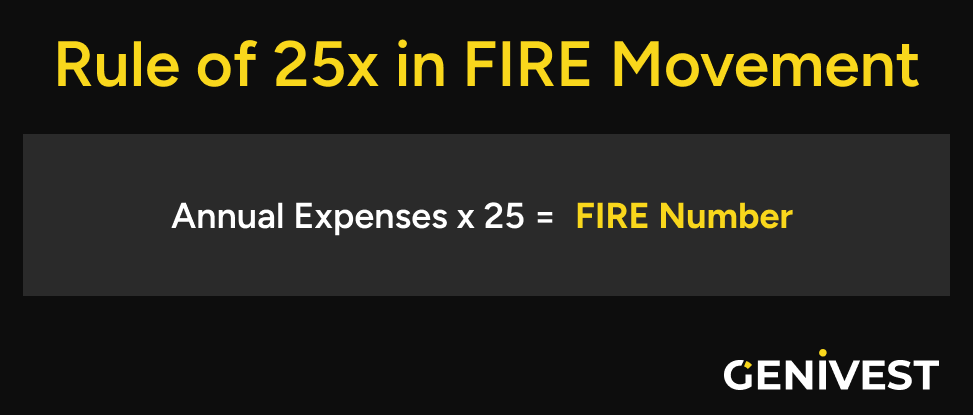

To achieve financial independence, there is a rule called the 25x rule. In this rule, you multiply your yearly expenses by 25 and accumulate an amount equal to your 25 years of expenses, which you then invest. This amount is usually enough to cover your expenses for the next 25 years, but if you get good returns on your investment, the number of years can increase even further.

After the first part, which is achieving “Financial Independence,” comes the second part, which is “Retire Early.” This part is optional, and it depends entirely on you whether you want to continue working or completely stop. You can also choose to work part-time; it completely depends on you.

How the FIRE Movement Began

The FIRE movement began a long time ago. Vicki Robin and Joe Dominguez wrote about it in their book “Your Money or Your Life” (1992). They explained that when you spend money, you are actually spending the time and energy of your life. The book emphasizes that by reducing expenses and increasing savings, financial independence can be achieved.

After that came the internet era, and bloggers like Mr. Money Mustache worked extensively on this concept and helped people understand it. As a result, the FIRE concept gained more popularity, and the FIRE community began to emerge.

Know Your FIRE Numbers: The First Step Toward FIRE

Before starting your FIRE journey, you should know your current financial situation. You can make a list of all your income sources, monthly expenses, debts, and assets. This will give you a clear picture of your current situation and help you understand how much you need to save and invest each month in the future. Knowing where you currently stand is the foundation of your FIRE plan.

FIRE Rule of 25x

When you understand your finances, the next step is to calculate your FIRE number. Your FIRE number represents the total amount you need to achieve financial freedom. You can easily calculate it using the 25x rule, which means multiplying your annual expenses by 25. For example, if your annual expenses are $25,000, your FIRE number will be $625,000.

To make this process easier, you can use our FIRE calculator. In this calculator, you need to provide your current savings, age, annual income, annual expenses, and expected rate of return. The calculator will then generate a complete report for you along with a comparison of your FIRE numbers.

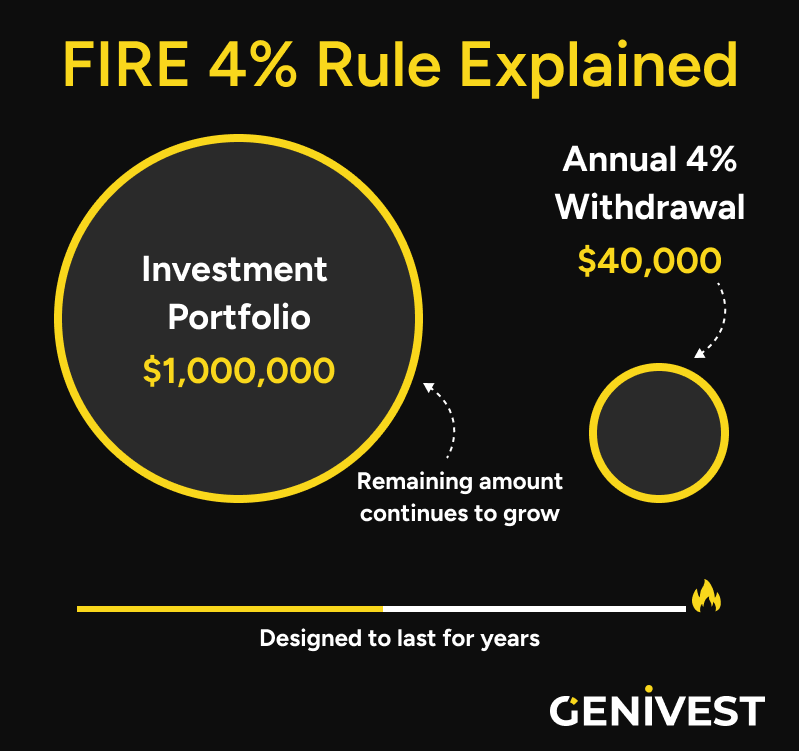

The FIRE 4% Rule Explained

The 4% rule helps you determine how much you can safely withdraw from your investment portfolio each year without running out of funds. According to this rule, you can withdraw 4% of your total investments annually to cover your living expenses. The remaining amount stays invested and continues to grow with inflation and market fluctuations.

For example, if you have invested $1,000,000, you can withdraw 4% ($40,000) annually. This amount is designed in such a way that you can sustain it for decades, provided you maintain a balanced portfolio and experience moderate market returns.

The 4% rule is closely connected to the 25x rule used to calculate your FIRE number. These two rules are actually the reverse of each other:

- The 25x rule tells you how much you need to save to reach financial independence.

- The 4% rule tells you how much you can safely withdraw once you get there.

Why It Matters

The 4% rule gives you a practical benchmark for financial planning. It helps you estimate whether your savings and investments can support your desired lifestyle after retirement or once you achieve financial independence.

However, it’s important to remember that the 4% rule is a guideline, not a guarantee. Market conditions, inflation, and personal spending habits can all affect your withdrawal rate. Many modern FIRE followers adjust this number to 3.5% or even 4.5% based on their comfort level and financial goals.

How Much Should You Save for FIRE?

The higher your saving rate, the sooner you will achieve your FIRE goal. For example, if you save 50% of your income, you can reach your goal in approximately 17 years. However, if your saving rate increases to 80%, you can achieve your FIRE goal in just 6 years.

The key idea behind the FIRE saving rate is to minimize expenses and maximize savings so your investments can grow enough to cover your annual living costs through passive income. This often involves budgeting strictly, cutting unnecessary spending, and focusing on long-term investment growth.

Track Your Expenses, Reach FIRE Faster

When you control your expenses, you actually regain control over your life and time. Expense tracking and budgeting help you understand where your money is going. The small daily expenses, when added up monthly or yearly, become a significantly large amount.

Start by tracking your expenses for an entire month. You can use any budgeting app, spreadsheet, or even a simple notebook. I have been using the Money Manager app for several years. The method doesn’t matter, consistency does. When you start recording your expenses, you’ll begin to notice your spending patterns, which you might not have been aware of before.

You can also try our Personal Budget Calculator to easily manage and analyze your expenses.

Categorize Your Expenses

Divide your spending into clear categories such as:

- Needs: Rent, utilities, groceries, transportation

- Wants: Entertainment, dining out, hobbies, subscriptions

- Savings & Investments: Money directed toward your FIRE goal

This categorization helps you identify where you can cut back without compromising your essential lifestyle.

Set Up a Realistic Budget

Budgeting doesn’t mean making your life difficult; rather, it means giving every penny a purpose. For this purpose, you can adopt the 50/30/20 rule (50% needs, 30% wants, and 20% savings) as a starting point and modify it according to your needs. The main goal is to stay flexible and achieve your FIRE goal.

Build Your Emergency Fund

Before starting your FIRE journey, you must first and foremost build an emergency fund. Because life is not always the same, unexpected situations can happen anytime. For example, losing a job, having a health issue, getting into an accident, or any natural disaster. Such emergencies can disturb your FIRE journey, forcing you to withdraw from your savings or investments. Due to market volatility, you might have to sell your assets at a loss, which can also delay your FIRE journey.

How Much Should You Save in an Emergency Fund?

Generally, you should save an amount equal to 3 to 6 months of your expenses in your emergency fund. If your income is stable, then a 3-month emergency fund may be sufficient. However, if your income fluctuates or you are self-employed or a freelancer, then you should build an emergency fund that covers at least 6 months of your expenses.

For example, if your monthly expenses are $2,000, then your emergency fund should be between $6,000 and $12,000.

| Marital / Family Status | Dependents | Income Source | Income Stability | Recommended Emergency Fund Duration | Explanation |

| Single, no dependents | 0 | Fixed salary job (govt/private) | High | 3 months | Low financial responsibility, stable income |

| Single, supporting parents | 1–2 | Fixed salary job | Moderate | 4–6 months | Some dependents, moderate cushion needed |

| Married, dual income | 0–1 | Both salaried | High–Moderate | 4–6 months | Two incomes reduce risk but need shared buffer |

| Married, single income | 1–2 | Salaried job | Moderate | 6–9 months | One earner supports family — higher risk |

| Married, kids & loans | 2+ | Salaried / business | Moderate–Low | 9–12 months | Family + EMIs = more pressure on cash flow |

| Self-employed / Freelancer (single) | 0–1 | Business / freelance | Low | 6–9 months | Variable income, need larger buffer |

| Self-employed / Freelancer (married) | 1–2+ | Business / freelance | Low | 9–12 months | Family + unstable income → strong safety net |

| Retired / Fixed pension | 0–1 | Pension / savings | High | 3–6 months | Stable but limited income, small buffer enough |

Where to Keep Your Emergency Fund

Your emergency fund should be liquid and easily accessible, but not mixed with your regular spending money. The best places to keep it include:

- High-yield savings account: Offers quick access with better interest than regular accounts.

- Money market account or short-term treasury fund: Slightly higher returns with low risk.

Avoid investing your emergency fund in stocks, crypto, or any volatile assets. The purpose of this fund is stability and accessibility, not growth.

Why an Emergency Fund is Crucial for FIRE

If you don’t have an emergency fund, even one unexpected expense can disturb your whole FIRE plan. Imagine you have to take money out of your investments during a market dip just to pay for a medical bill. This not only reduces your savings but also slows down your long-term growth.

An emergency fund helps protect your investments and gives you peace of mind. It makes sure you are ready for life’s surprises while staying on track toward financial independence.

FIRE Strategies

Now the next important step is to achieve the FIRE number as soon as possible. For this, you can use different strategies. By using these strategies together, you can achieve your FIRE number quickly.

Increase Your Income

The higher your income is, the more you can increase your saving rate and the more you can invest. You will have to take action to increase your cash flow.

- Career Improvment: If you do a job, you can improve your skills and negotiate for a higher salary. Or you can look for jobs that offer a higher salary.

- Side Hustle: Along with your job, you can also do a side hustle to increase your income. This can be freelancing, YouTube content creation, affiliate marketing, blogging, graphic designing or ride sharing. It depends on what you can do easily, your geographic location, and your personal situation.

Decrease Your Expenses

Increasing income is an offensive strategy, while reducing expenses is a defensive strategy. It is easier to control and has a greater impact.

- Mindful Frugality: This is not about deprivation; it is about spending wisely. Differentiate between your needs and wants, and eliminate those expenses that do not bring you real happiness or value.

- Attack the Big Three Expenses: Usually, the largest portion of any budget consists of housing, transportation, and food. Reductions made in these areas provide the greatest savings.

- Housing: Renting out rooms in your house (house hacking), moving to a smaller home, or relocating to a lower-cost area.

- Transport: Instead of financing a new car, drive an old, reliable car, use a bicycle, or use public transport.

- Food: Cooking at home, meal planning, and eating out less at restaurants.

- Avoid Lifestyle Creep: As your income increases, resist the desire to increase your expenses. Instead, put every raise and bonus directly into your investments.

Start Investing

The biggest enemy of money is inflation. If you keep saving money, its value decreases every year. The percentage of inflation can vary in every country. But if you want to grow your wealth, you have to put every single penny to work.

- The Magic of Compounding: Understand compound interest as “earning interest on interest.” It is the power that allows your portfolio to grow exponentially over time. Even a small amount, when compounded over a long period, can turn into a large fortune. Use our Compounding Calculator to find out how your money can grow with time and consistency!

- Investing Methods For FIRE:

- Low-Cost Index Funds and ETFs: These are the favorite investments of the FIRE community. They allow you to invest in the entire market, are passively managed, and have extremely low fees, which maximize your returns over the long term.

- Stocks and Bonds: These are the basic assets of most funds. The allocation between them depends on your risk tolerance and time horizon.

- Real Estate: It can provide passive income through rent and the potential for appreciation in value.

- Tax-Efficient Investing: Contribute as much as possible to tax-advantaged retirement accounts to let your money grow without the burden of taxes.

These three strategies of FIRE are not independent, rather they form an interconnected feedback loop of mutual reinforcement. Progress in one area enhances the performance of the others. For example, reducing your expenses not only increases your savings rate but also permanently lowers your future FIRE number. Cutting $100 in monthly expenses saves you $1,200 annually, and according to the 25x rule, it reduces your total FIRE number by $30,000 ($1,200 x 25). This “double effect” is a powerful concept. Every dollar you don’t spend is a dollar you can invest, and a dollar you won’t need to fund for the rest of your life in retirement. Understanding this interconnection can accelerate your FIRE journey to an unbelievable extent.

FIRE Variations and What They Mean

FIRE is not a rigid, one-size-fits-all approach. Over time, it has evolved into a flexible spectrum that makes its principles practical according to different goals and lifestyles. This means you can find a path between extreme frugality and complete retirement that works best for you. This section will explain the different types of FIRE so that you can make the best choice according to your financial goals and personal values.

Lean Fire: The Path of Frugality

- Goal: To retire as early as possible by adopting extreme frugality and minimalism. In this, the retirement lifestyle is simple, with annual expenses (in the context of the U.S.) often being less than $40,000.

- Who It’s For: For those who value time and freedom more than material possessions and can live happily on a tight budget. Lean FIRE means living on less so that you can gain freedom from work sooner.

Coast FIRE: Let Compounding Do the Work

- Goal: To save and invest aggressively in the early stages of your career until your portfolio becomes large enough that, without any further contributions, it will automatically grow to your full FIRE number by the traditional retirement age (for example, 65 years).

- The “Coasting” Phase: When you reach your “Coast FI” number, you only need to work to cover your current expenses, which frees you from the pressure of saving for retirement.

- Who It’s For: For those who want to reduce financial stress during the middle years of their career while still ensuring a secure traditional retirement. It allows you to work hard in your youth and relax in your old age.

Barista FIRE: Hybrid Approach

- Goal: To save enough money to cover most of your expenses, and then leave a high-stress, full-time job to do part-time work of your choice (such as being a barista, hence the name). This part-time income supplements the amount withdrawn from investments and often also provides benefits like health insurance.

- Who It’s For: For those who do not want to completely stop working but desire more control, flexibility, and a better work-life balance. It is a pleasant combination between “retirement” and work.

Fat FIRE: Retirement in Luxury

- Goal: To retire early without sacrificing a high standard of living. This requires a very large amount of wealth to cover annual expenses of $100,000 or more.

- Who It’s For: For high-income professionals (doctors, lawyers, entrepreneurs) who can save aggressively while maintaining a comfortable lifestyle. Fat FIRE provides both freedom and luxury.

Asset Allocation for FIRE Investors

Asset allocation simply means deciding how much percentage of your total portfolio you will invest in different asset classes such as stocks, bonds, real estate, cash, and others. Each asset class has a different risk level, return potential, and time suitability.

The right mix ensures that your money grows steadily while also being protected during market downturns. To find the perfect mix for your goals, try our Asset Allocation Calculator now!

Why Asset Allocation Matters

- Risk Control: It spreads your money across various investment types so that if one underperforms, the others can balance it out.

- Consistent Growth: A diversified portfolio reduces volatility and ensures smoother long-term returns.

- Goal Alignment: Your allocation should match your time horizon, short-term goals need safer assets, long-term goals can handle more volatility.

| Asset Type | Risk Level | Return Potential | Liquidity | Suitable For | Ideal Time Horizon | Example Instruments |

| Cash / Savings | Very Low | Very Low (1–3%) | Very High | Emergency fund, short-term needs | 0–2 years | Savings account, Money market funds |

| Bonds / Fixed Income | Low–Moderate | Low–Moderate (3–6%) | Moderate | Stability & steady income | 2–7 years | Government bonds, corporate bonds, fixed deposits |

| Stocks / Equities | High | High (7–12% or more) | High | Long-term growth, wealth building | 7+ years | Index funds, ETFs, individual stocks |

| Real Estate | Moderate–High | Moderate–High (6–10%) | Low | Passive income, inflation hedge | 10+ years | Rental properties, REITs |

| Gold / Commodities | Moderate | Moderate (4–7%) | Moderate | Hedge against inflation | 5+ years | Physical gold, Gold ETFs, commodities funds |

| Crypto Assets | Very High | Very High (10%+) | High | Speculative, high-risk investors only | 5+ years | Bitcoin, Ethereum, crypto ETFs |

Sample Asset Allocation Based on Risk Appetite

| Investor Type | Risk Tolerance | Stocks / Equity | Bonds / Fixed Income | Real Estate | Gold / Commodities | Cash / Short-Term |

| Conservative | Low | 20% | 50% | 10% | 10% | 10% |

| Balanced | Moderate | 40% | 30% | 15% | 10% | 5% |

| Aggressive | High | 70% | 10% | 10% | 5% | 5% |

Rebalancing Your Portfolio

Asset allocation is not a one-time task. Market movements can shift your percentages for example, if stocks rise sharply, they may occupy a larger share of your portfolio than intended.

That’s why it’s important to review and rebalance your portfolio once or twice a year to bring it back to your target allocation.

Pros and Cons of the FIRE Movement

Like any financial strategy, the FIRE (Financial Independence, Retire Early) movement has its own advantages and challenges.

It is not a get-rich-quick scheme; it is a long-term lifestyle change that requires discipline, patience, and clear goals.

Let’s explore both sides of FIRE to understand its strengths and weaknesses.

Pros: Why FIRE Can Transform Your Life

- Financial Freedom: The biggest benefit of FIRE is true financial independence. You work because you want to, not because you have to. It gives you complete control over your time and choices.

- Less Stress and Job Security Anxiety: Once your investments cover your living expenses, you no longer worry about losing your job or facing financial instability. That peace of mind is invaluable.

- More Time for What Matters: FIRE allows you to spend your time doing what you love, such as traveling, learning, family time, creative projects, or volunteering.

- Mindful Spending and Minimalism: FIRE encourages you to spend intentionally. You focus on things that bring real happiness instead of unnecessary material possessions.

- Power of Compounding: By saving and investing early, you take full advantage of compounding. Your money grows faster over time and helps you reach financial independence sooner.

Cons: The Challenges of FIRE

- Aggressive Saving Can Be Difficult: Saving 50 to 80 percent of your income is not easy. It requires lifestyle sacrifices, strict budgeting, and saying no to some luxuries.

- Market Dependence: FIRE depends heavily on investment returns. Market downturns or inflation can reduce your portfolio’s value and delay your goal.

- Lifestyle Creep Risk: If your expenses increase after reaching FIRE, your portfolio may not last as long as planned. Staying disciplined is essential.

- Loss of Job Benefits: Leaving your job early can mean losing benefits such as health insurance, retirement contributions, or paid leave. These need to be managed separately.

- Boredom or Lack of Purpose: Some people feel lost after early retirement. Without structure or a clear purpose, it can lead to boredom or dissatisfaction.